|

In view of the interest

aroused by the passing- of the National Insurance Amendment Act, 1913,

which became law on 15th August, 1913, the following notes may possibly

be regarded as in some degree helpful in eliminating certain

difficulties attendant upon an initial consideration of its provisions

as affecting Scotland.

The Employed

Contributor.

A very important

concession has been granted to such persons by the extension until 13th

October, 1913, of the period within which advantage may be taken of the

right to enter into full insurance at the flat rate of contribution.

All employed contributors

entering into insurance before that date will do so at a uniform rate of

contribution, while those who become employed contributors after 13th

October will require to pay a rate appropriate to their age at entry or

suffer an equivalent reduction of benefit.

A very important

alteration has been made with reference to the sickness benefit payable

to insured persons of age 50 and upwards. Under the principal Act such

persons were subdivided into four distinct classes :—

(a) Persons between 50

and, 60.

(b) Persons between 60

and 65.

(c) Persons between 65

and 70 as at 15th July, 1912, who entered into insurance prior to 15th

July, 1913.

(d) Persons under 65 at

15th July, 1912, who did not become employed within the meaning of the

Act until after attaining age 65.

These various classes

were dealt with as follows :—

Classes (a) and (b)

received substantially reduced sickness benefit.

Class (c) received only

such benefit as their Societies might determine.

Persons in class (d) were

not allowed to be insured or to receive any benefit, but their employers

were required to contribute 5d. per week in respect of them.

All these restrictions

have now been swept away, and persons in the four classes referred to

may now become insured persons enjoying the same rates of benefit as

other employed contributors. The only qualification now existing is that

persons who become employed contributors, after attaining age 65, shall

not be entitled to medical benefit after age 70 unless at least 27

contributions have been paid in respect of them.

A new class of employment

has been brought within the scope of the Act’s compulsory provisions,

viz., “Employment under any local or public authority except such as may

be excluded by a special order.”

Employed contributors

over 60 may, if they have ceased to be so insurable and if they are

otherwise qualified to do so, become voluntary contributors at any time

irrespective of the duration of their insurance as employed

contributors. The rate of contribution exigible in such case continues

to be the employed rate. Under the principal Act this privilege was

allowed only to employed contributors who had been insured as such for

at least five years.

The Voluntary

Contributor.

The period during which a

voluntary contributor under age 45 may come into insurance at the flat

rate has been extended to 13th October, 1913. This provision will

necessitate the allowance of special credits in respect of excess

contributions during the period between 15th January and 13th October,

1913.

No voluntary contributors

whose income from all sources exceeds 1 GO will be entitled to receive

medical benefit, but if in insurance their weekly contributions will be

reduced by one penny.

Exempt Persons.

A new class of exempt

persons has been created. Any person who proves that he is ordinarily

and mainly dependent for his livelihood on the earnings derived by him

from an occupation which is not employment within the meaning of the Act

is entitled to a certificate of exemption. This provision meets the

case, for example, of the certificated teacher under a pension scheme

who may take a class in an evening school.

Another of the provisions

of the new Act is that which confers upon exempt persons the right to

receive medical and sanatorium benefit, subject only to certain

qualifying conditions to be imposed by the Commissioners.

It is expressly

stipulated that exempt persons whose annual income from all sources

exceeds ^160 shall be required to make their own arrangements for

medical treatment. A proportionate payment will be made to them out of

funds reserved for this purpose.

Aliens.

The position of women

who, prior to their marriage with an alien had been British subjects,

has now been materially improved. Formerly the State proportion of the

cost of benefit was denied them, but now such a married woman is

entitled to receive full benefits if she is herself insured and whether

or not she is so insured the maternity benefit payable in respect of her

alien husband’s insurance is increased by two-sevenths. The cost of this

increase is defrayed out of moneys furnished by Parliament.

The effect of this

provision is that a British woman’s rates of benefit remains unaltered

for insurance purposes even although she marries an alien.

Aged and Infirm

Members of Societies.

All members of Societies

as at lGth December, 1911, who were not qualified to become insured

persons by reason of age or permanent disablement and who were then

entitled to medical attendance and treatment are to receive medical

benefit as from 12th January, 1914. This privilege was formerly confined

to members of such Societies as became approved, but the restriction has

now been removed. Parliament contributes towards the cost of medical

treatment for this class the same proportion as that provided in the

case of ordinary insured persons.

Seamen.

Dissatisfaction was

formerly caused by the fact that the Seamen’s National Insurance Society

could not admit to its membership masters, seamen and apprentices to the

sea-service, or the sea-faring service, who were qualified to become

voluntary contributors. This power has now been granted and it is

anticipated that some fishing boat owners and other sea« faring men, not

employed under contract of service, will avail themselves of the

benefits secured by this provision.

It is also provided that

where a shipowner—although liable to provide maintenance and medical

treatment—is not liable to pay wages, a Society shall have power, in the

case where the seaman was serving on a home trade ship, to apply

sickness benefit in whole or in part for the benefit of his dependants.

Maternity Benefit.

Perhaps the most widely

discussed clause during the passage of the Bill through Parliament was

that dealing with

Maternity Benefit. Its

provisions may be briefly outlined as follows :—

Maternity Benefit is now

in all cases regarded as the mother’s benefit, her receipt alone being

regarded as a valid discharge to the Society or Committee concerned. The

husband’s receipt, on her behalf, may be accepted if authorised by her.

The position where the

husband alone is an insured person otherwise remains unchanged, but in

all cases where the wife is herself an insured person, and a Society

member qualified for benefit, double maternity benefit of £3 is payable.

If the husband is a

Society member and entitled to maternity benefit half of this sum is

paid in respect of his insurance. If he is a deposit contributor, as

much of the 30s. as his account will bear is advanced, and the balance

is made good by the wife’s Society, otherwise the entire cost of

maternity benefit is borne by the latter Society.

It will be observed that

the anomaly previously existing in the case where husband and wife were

both insured persons, but the husband was unqualified for maternity

benefit, has now been removed.

It should be noted that

where any benefit is paid in respect of the wife’s insurance, she is

required to abstain from remunerative work during a period of four weeks

after her confinement. The position of maternity benefit under the Acts

may thus be summarised :—

(a) Husband .insured,

wife not insured—husband’s society pays one benefit to the wife.

(b) Husband and wife both

insured—husband’s and wife’s society each pay one benefit to the wife.

(c) Wife insured, husband

not insured—wife’s society pays two benefits to her.

'd) Unmarried insured

woman—her society pays her one benefit.

Arrears.

Of the provisions

affecting- the practice of Approved Societies, those dealing with the

treatment of arrears incurred during periods of unemployment must be

regarded as particularly worthy of notice.

The hardship entailed

upon members of Approved Societies in having to pay not only their own

but also their employers’ contribution during unemployment has

frequently been adversely criticised.

In terms of the principal

Act the employers’ share of contributions might be disregarded, but only

at the discretion of the Society. In the new Act it is explicitly laid

down that an employed contributor falling into arrears requires to make

payment only of his own share of the contributions, and fot-the purpose

of determining this share the rate of remuneration, except where

sufficient evidence to the contrary is adduced, is deemed to exceed 2s.

6d. per working day. Thus a man who has been out of work for 15 weeks

requires to pay only 15 x 4d., or 5s., in order to come back into full

benefit, instead of 15 x 7d., or 8s. 9d., as formerly.

The loss to Societies in

excess of an average of three full weeks’ contributions per member per

annum is to be made good out of the sums retained for cancellation of

reserve values. If the aggregate amount so payable in any year exceeds

^100,000 this excess is to be met out of moneys to be provided by

Parliament.

It is proposed that

instead of permitting arrears to accumulate from year to year, the rate

of sickness benefit payable to the defaulting member should during each

year be reduced roughly in proportion to the value of the loss incurred

by the Society from his failure to pay contributions during the

preceding year. This reduction of benefit will be based upon the

expectation of sickness of the individual. Thus a man of 40 would

require to forego, say, 6d. a week of sickness benefit for one year for

every contribution in arrear during the previous twelve months. That is

to say, this man, if 12 weeks in arrear would suffer reduction of

sickness benefit to the extent of Gd. x 12, or 5s. per week; but

provided that he incurred no further arrears during the year of

reduction he would come automatically into full benefit as from the end

of that year.

The corresponding

reduction in the case of a man presently aged 55 would be, say, 3d. per

w’eek.

Tables will doubtless be

calculated shewing the value of arrears at various ages, and an

examination of these tables will at once reveal the precise position of

the individual member to the member himself and to the Society Secretary

responsible for the administration of his benefits.

Before leaving this

topic, it may be pointed out that if in any year more than 48

contributions are paid in respect of any member, these excess

contributions will be held to his credit and will be utilised in wiping

out any arrears of contributions which may subsequently accrue in

respect of him.

Sickness Benefit.

Other modifications of

the provisions affecting the administration of sickness benefit may here

be briefly referred to :—

Continuing Sickness.

The requirement that 50

contributions must be paid between two periods of illness to prevent

them being regarded as continuous is now dispensed with. It is still

necessary, however, that a period of at least 52 weeks should intervene.

Waiting Period.

“Commencing on the fourth

day of such incapacity ” is to be substituted for “ commencing from the

fourth day after being so rendered incapable of work.” A day upon which

the incapacitated person was prevented by the incapacity from doing any

effective work is to be treated as a day of incapacity, but Sunday is

not deemed one of the three working days which must elapse, unless the

insured person would, but for his incapacity, have actually been

employed upon that day.

Members in Hospital.

The provisions of the

principal Statute dealing with the treatment of sickness benefit while

the member is in hospital have been somewhat modified. It is now laid

down that where no payment, or partial payment only, of Sickness Benefit

has been made— /

(a) To his dependants, or

if he had no dependants,

(b) to the Insurance

Committee,

(c) under a previously

existing agreement to the hospital authorities ; the money so withheld

shall be applied—

In the provision of

surgical appliances or otherwise for his benefit after he ceases to be

an inmate, or if not so expended shall be paid in cash, in a lump sum,,

or in instalments, to the member after leaving the institution.

Member in receipt of

compensation under Workmen’s Compensation Act, 1906.

Where an insured person

is receiving reduced sickness allowance, representing the difference

between full sickness benefit and the sum payable in accordance with the

provisions of an agreement under the Workmen’s Compensation Act, the

amount paid in sickness benefit shall be totalled and the number of

weeks during which he shall be deemed to have received sickness benefit

will be reckoned by dividing this total by the full weekly rate of

benefit. For example, suppose that the insured person has during the

first period of illness received a compensation allowance of 7s. 6d. per

week and sickness benefit of 2s. 6d. per week. If now it be assumed that

these sums were paid for 16 weeks and that at some later period during

the same year the insured person again falls ill, it is necessary to

reckon the period during which full sickness benefit can be allowed. The

period during which full benefit was formerly paid is consequently 2s 6d

/ 10s x 16, or 4 weeks, and the insured person is therefore entitled to

full sickness benefit during the further period of 22 weeks.

This, it should be

observed, applies only in the case where the member recovers and

subsequently becomes ill. In the case of a continuous illness, however,

each week during which any payment is made counts as a full week towards

the 26 weeks throughout which benefit is payable.

International

Societies.

Several most important

administrative changes are made by the Clause dealing with international

Societies. Previously, the members of such Societies resident in each

part of the United Kingdom were required to be treated for the purposes

of valuations, surpluses, deficiencies and transfers as if they formed a

separate Society. These provisions have now been done away with.

Fortunately, however, it is provided that if application to the Joint

Committee be made before 15th February, 1914, Scottish members of such

Societies may continue to be regarded as constituting separate

societies. Thanks to this Clause, Scottish members will, if immediate

action is taken, be entitled to preserve for their own benefit any

surpluses expected from the higher sickness rates or better management

which may prevail in Scotland. If this option be not exercised, it is

obvious that if there are surpluses derived from the contributions of

Scottish members, these will be utilised to set off in some degree any

less favourable conditions experienced in the administration of sickness

benefit in the sister countries.

It cannot therefore be

too strongly urged that Scottish members should immediately consider the

whole position in the light of the conditions appertaining to their

entry into insurance and to the potential possibilities of Scottish

experience and management. The first step should take the form of

availing themselves, through their branch Societies, of the proviso of

Section 16 (1). If it is further wished to have districts separately

valued in Scotland, the second step would then be to apply under Section

40 of the original Act for association m geographical areas if their

rules permit. If they do not so permit, they should be altered.

This would result in

achieving a separate valuation from England. Each of the groups

exceeding 5,000 would also be valued separately in Scotland. If the

proviso of Section 16 (1) is not excepted, then deficiencies or

surpluses will be pooled with England. If the proviso is generally

accepted such pooling is confined to Scotland. Such a process would keep

the whole country (i.e., Scotland) together, would keep the whole

Societies together, and still allow for local autonomy.

Insurance Committees.

Insurance Committees are

now constituted bodies corporate and power is given them to take,

purchase and hold land for the purposes of the National Insurance Act.

They are also empowered under certain conditions (in accordance with a

scheme to be submitted for the approval of the Commissioners) to pay to

their members subsistence allowances and compensation for loss of

remunerative time caused by necessary attendance at Committee meetings.

Committees are also

authorised to subscribe to any association of insurance Committees whose

objects are approved by the Commissioners, and to pay reasonable

expenses incurred by their representatives in attending meetings of such

associations.

In conclusion, the

following miscellaneous provisions may be noted :—

Proceedings for

non-compliance with the provisions of the Act and its regulations may be

taken at the instance of the Procurator Fiscal or of the Scottish

Insurance Commissioners.

Stamp Duly is no longer

exigible in respect of certain documents frequently required in the

operation of the Act.

Certificates of marriage

required for production in connection with applications for maternity

benefit are now obtainable for a fee of 1s.

An Approved Society may,

notwithstanding that its membership is less than 50 or more than 5,000,

join an association of Societies for valuation purposes.

Scottish County Councils

are empowered to borrow on security of the General Purposes Rate in

order to obtain funds for the erection of sanatoria, and can now

purchase and lease land. County Councils, which have been authorised to

provide sanatoria, have now received the same powers of providing

treatment for all persons suffering from tuberculosis as were formerly

possessed by local authorities for the treatment of infectious diseases.

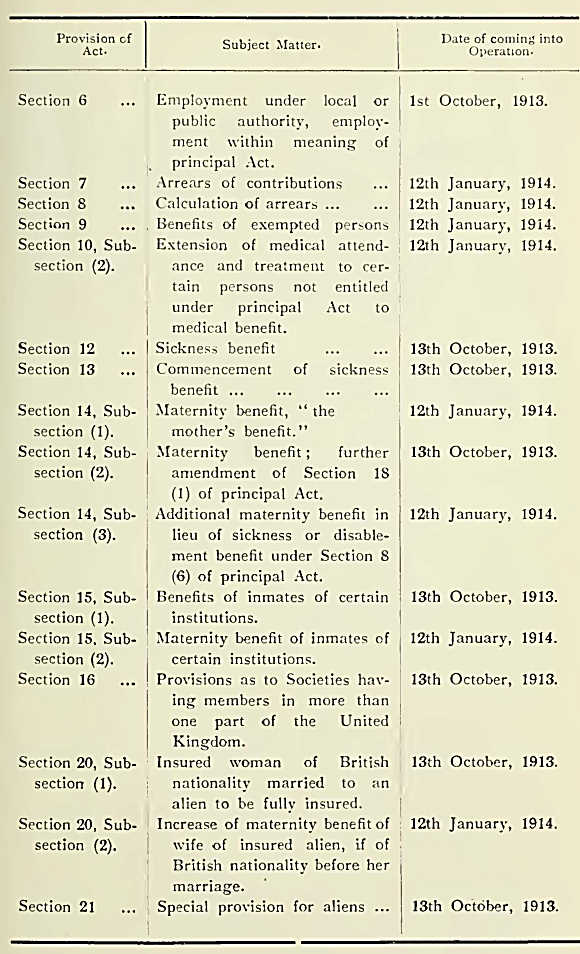

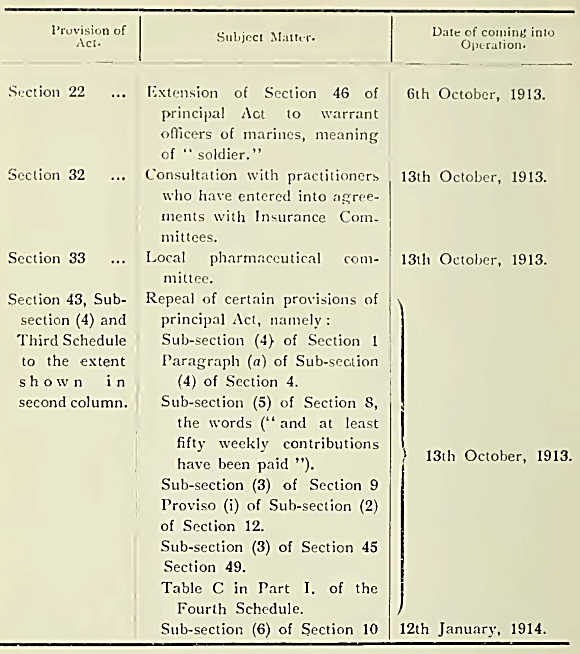

The appended Schedule

gives particulars of the dates upon which the various provisions of the

new Act come into operation.

|