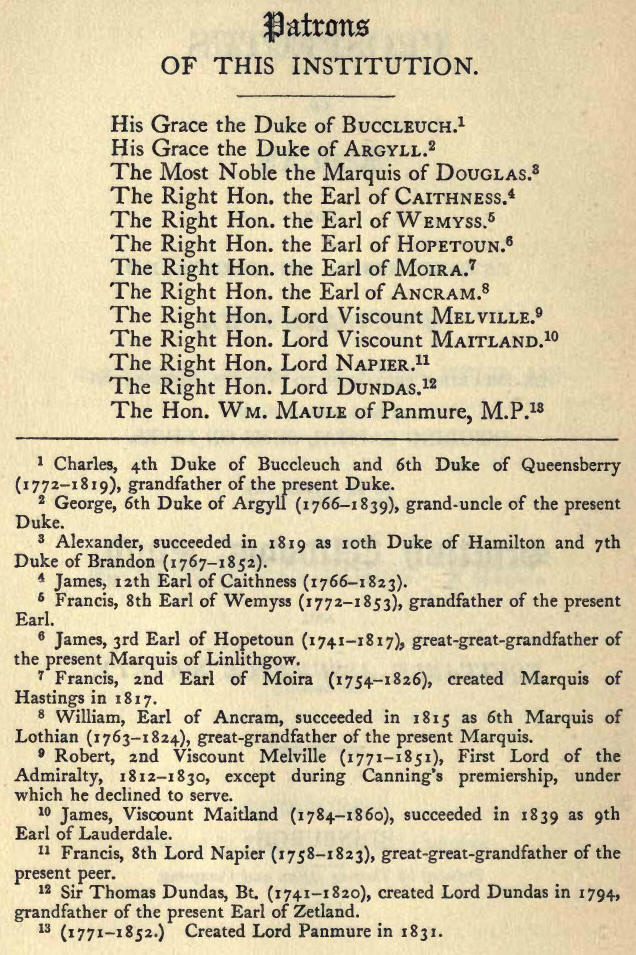

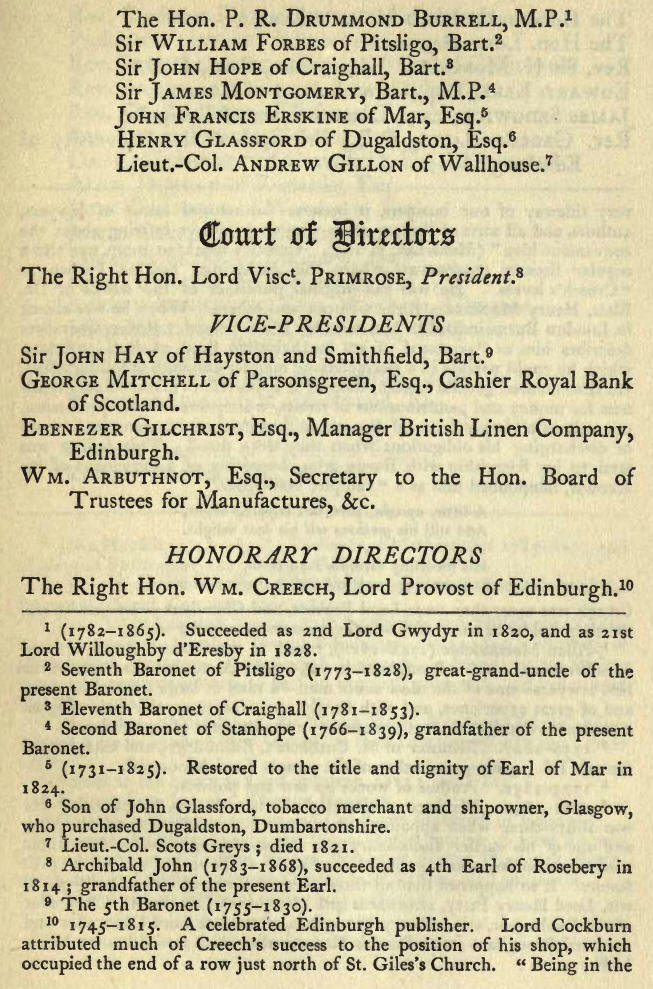

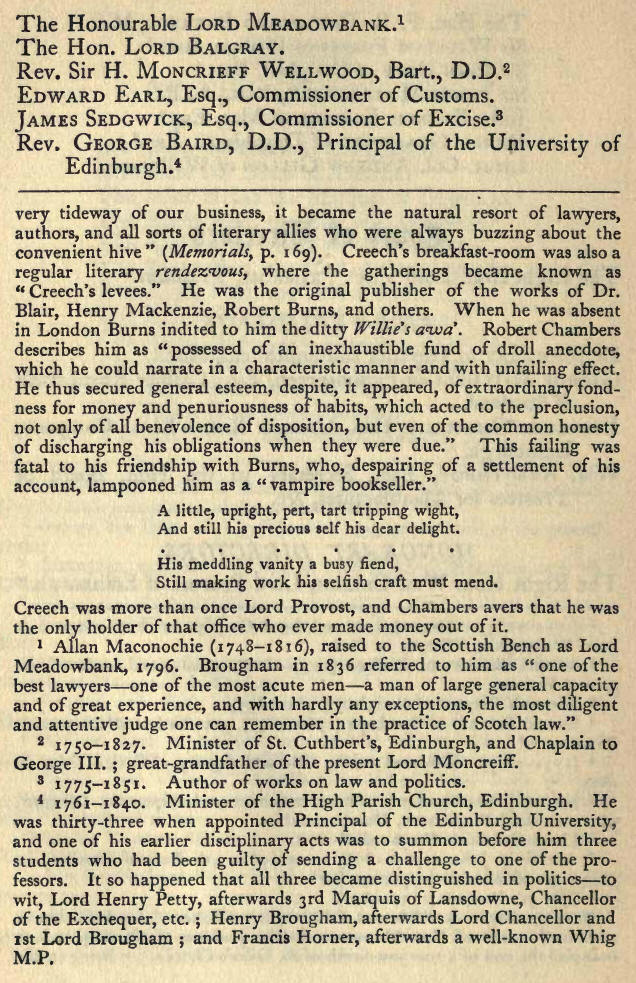

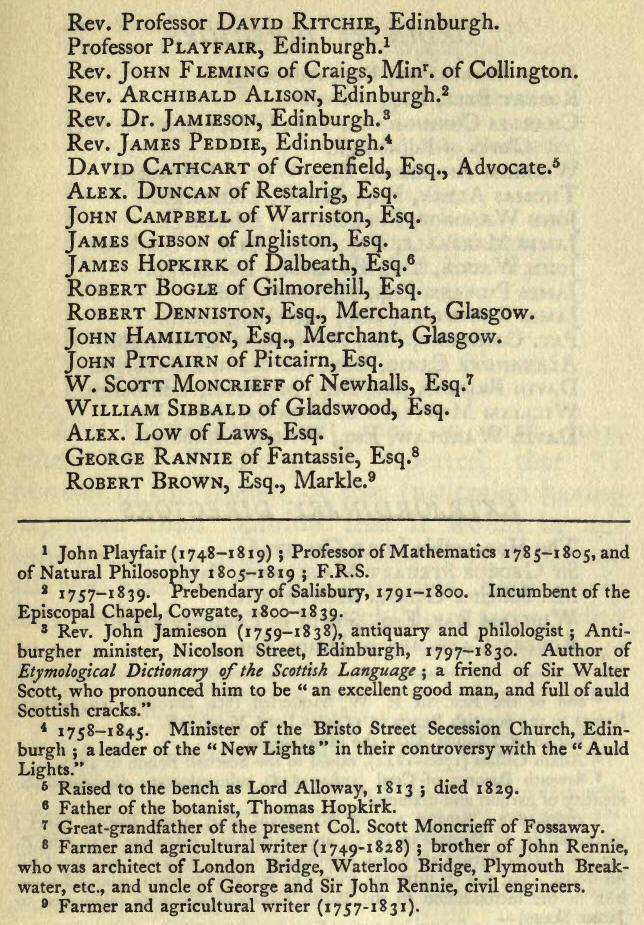

|

Multa fidem promissa levant, ubi plenius aequo

Laudat venales qui volt extrudere merces. [1]

1 He who overpraises the goods he wishes to dispose

of; shakes our confidence by his lavish promises.—Horace, Ep. ii. 2. 10.

He sinks in credit who attempts to raise

His venal wares with over-rating praise,

To put them off his hands. Francis's

Translation.

So wrote Horace, and a later cynic pronounced

promises to be like pie-crust--made to be broken. But there are promises

and promises, and an Institution which has made upwards of one hundred and

forty-six thousand promises and has never failed in fulfilling any one of

them, may be held entitled to the confidence of its members and the

public.

Such is the record of the SCOTTISH WIDOWS' FUND LIFE

ASSURANCE SOCIETY, the oldest life

office in Scotland. [The Hercules Fire Office

undertook life assurance in Edinburgh in 5809, but gave it up after a very

brief experience. In a publication by the Edinburgh Life Assurance Company

in 1908 it is claimed for that honourable corporation that it is "the

oldest office transacting life assurance, endowment and annuity business

alone—without fire, marine or other risks —which affords the additional

security of a substantial capital (£500,000)." It is to be noted that,

while this is quite consistent with the fact that the Scottish Widows'

Fund is the oldest life office in Scotland, a dividend has to be paid to

shareholders in the above capital of half a million sterling, whereas in

the Scottish Widows' Fund—a purely mutual society—there are no

shareholders and the whole profits are divided among policy-holders, whose

security rests, not on shareholders' property, but on their own invested

funds of £21,000,000,] which, since its foundation one hundred years ago

has issued upwards of 146,000 policies of assurance, and has met every

obligation arising therefrom.

A good deal of wisdom is sometimes compressed into

pithy saws. "Gang forward!" is a gallant motto, long since adopted by the

Stirlings of Keir; but "Gang warily!" is a wiser one, appropriated by the

Drummonds; and it was in that spirit that Scottish men of business acted

in the matter of life assurance. During the closing years of the

eighteenth century, when assurance companies were rising like mushrooms in

London, and, with few exceptions, perishing as quickly, our Scottish

forebears were quietly biding their time, accumulating knowledge from the

experience of their more venturesome fellow-subjects in the south.

It did not, however, escape the observation of

certain shrewd minds that the agents of English assurance companies on a

proprietary basis had become pretty busy in Scotland and were securing a

considerable amount of business. The attempt in 1809 of the Hercules

Society to undertake life assurance in Edinburgh, and its failure, were

not conclusive as to the possibility of establishing in Scotland an

institution similar to the Equitable, whereof the soundness and success

could not fail to be recognised [The Equitable Society was established

under the name of the Society for Equitable Assurances on Lives and

Survivorships. Although it was the first office to graduate premiums

according to the age of insurers, for very many years after it began

business it took lives without medical examination or certificate.

Candidates for assurance appeared before the Board, who questioned them

"as men of the world" ; and the success of the Society was proof that this

method was satisfactory.] for the Hercules was a proprietary concern, and,

when it abandoned its essay in life assurance, continued to conduct its

fire business in a manner profitable both to shareholders and clients.

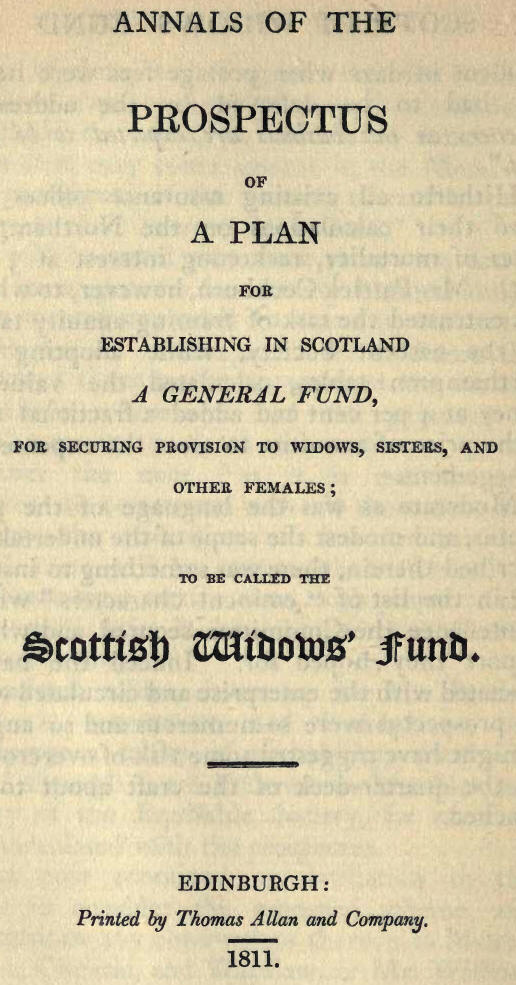

The credit of initiating a movement for the

establishment of a Scottish society was due to Mr. David Wardlaw, writer,

of Gogar Mount, who, in co-operation with Mr. Patrick Cockburn, drew up a

prospectus and "Plan of the Regulations" in 1811. This was submitted on

25th March 1812 to a small gathering of gentlemen who had been induced to

take an interest in the proposal, in the Royal Exchange, Edinburgh.

Mr. John Francis Erskine of Mar was called on to

preside, and the following gentlemen were nominated a Committee "to make

such enquiries and investigations as they shall find necessary for

enabling them to report to an adjourned meeting such regulations and

tables as they shall think proper to be adopted in commencing the

Institution "

This Committee held meetings on 6th and 21st April ;

and on the latter day, having obtained the opinion of the

Solicitor-General and Mr. Cathcart that the articles of a draft prospectus

which was before them would be "sufficient to exclude any risque of

general liability of members of the Society," they drew up an amended

prospectus, directing that it should be printed and circulated among "all

the principal towns and populous districts in the country and to all the

clergymen in Scotland, both of the Establishment and Secessions."

The prospectus was prefaced by the following

statement, setting forth the object and scope of the proposed Society.

The beneficial effects of the establishment for

making provision to Widows of the Clergy of the Church of Scotland have

been long felt and acknowledged, and have given rise to similar

institutions, which have also been attended with the most salutary

consequences; but all these being confined to particular districts,

societies, and corporations, it has occurred to some gentlemen in

Edinburgh to propose the formation of a General Society, with similar, but

more enlarged, views, the benefit of which may be extended to all parts of

the United Kingdom.

This proposition being highly approved of, and

patronised by some of the most eminent characters, the following plan has

been prepared, and is now humbly submitted to the consideration of the

Public.

It is unnecessary to dwell on the general advantage

of institutions which are calculated, by a small annual sacrifice when

persons are best able to spare it, to rescue from probable want and

dependence those beings whose permanent comfort every good man feels it to

be one of the first objects of his existence to secure.

Those who are unable to set apart such a portion of

their incomes as will afford, after their deaths, suitable annuities to

their widows or other dependent relations, have the satisfaction, by

joining such institutions, to feel that this great object is attained;

while the rich are saved the necessity of laying aside and securing

capitals for jointures or annuities, and enabled to leave them their

estates in so far clear and unembarrassed with what so frequently

happens—a tedious, troublesome, and expensive trust-management.

The principle of the proposed Institution is to take

from contributors no more than what, according to the most approved

calculations, is sufficient, by careful accumulation of the funds, to

afford the annuities contracted for, excluding any idea of proprietorship

or advantage to particular individuals; and it will be a fundamental rule

that the whole business of the Society shall be managed by persons

deriving their appointments from the free choice of the Members

themselves.

Among the rules drawn up by the Committee a few

points which are of interest at this day may be recapitulated.

Under Rule II. it is provided "that the Association

shall comprehend ALL RANKS." Unmarried men might nominate at their

admission "sisters or other females, who shall be considered on the same

footing as wives in respect to this establishment."

Profane persons might construe the privilege thus

offered to bachelors in regard to "other females on the same footing as

wives" in a sense very different from that contemplated by the reverend

chairman and the serious citizens composing his committee; but—Honi soit

qui mal y pense!

Rule III. sets forth that "any Member may secure

annuities to different Females, not exceeding, in whole, £500 a year on

the life of one Member, beyond which it is not proposed at present to go."

Rule IV.—No person to be admitted a Member who is

above sixty years of age, or whose wife is more than twenty years younger

than' himself. Presumably this limitation was intended to apply also to

the "different Females" provided for under Rule III.; anyhow the Directors

took power, "in all cases, to refuse applications of proposed Members

without assigning reasons." This was made all the easier by Rule V., which

laid down that Members were to be admitted by the Directors voting by

ballot, one blackball in three excluding a candidate.

Rule VII.-"The Widows of persons committing suicide,

falling by the hand of justice, or dying on the seas (except in His

Majesty's packets passing between Great Britain and Ireland) shall only be

entitled to annuities corresponding to the value of the interest of their

husbands at the time of their deaths."

Surrender values were provided for under Rule XXII.,

which empowered the Directors, "for behoof of the Society, to buy up the

interest of any of the Members wishing to dispose of the same, in whole or

in part"; and under Rule XXVIII. it was ordained that "if, in process of

time, it shall appear that the Society shall have acquired a capital more

than sufficient to uphold its credit, as well as to satisfy all claims

that may come against it, the Members shall participate of the benefits

thereof in proportion to their interests in the fund."

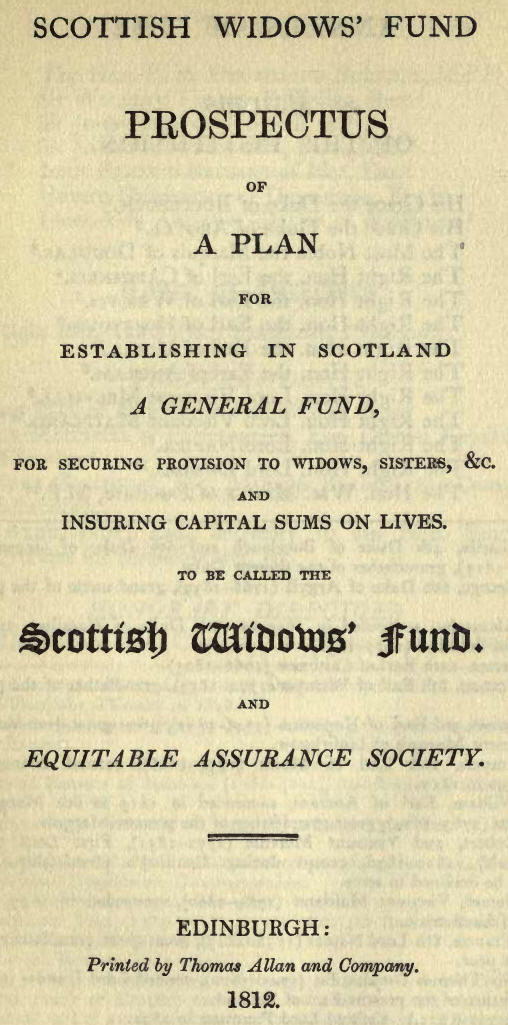

It will be noted that these rules were drawn up so

as to provide for annuity business only; but in a note appended to them it

was stated that it was in contemplation so to frame the Articles of

Constitution as to extend the scheme to include endowment and the payment

of capital sums on the death of members. "But," continues the note, "as it

is not thought expedient to commence with all these branches at once, the

execution of that for insuring capital sums will be postponed, or limited

to small sums for a certain time, with power to the Directors to defer it

for a longer time, if they shall think proper."

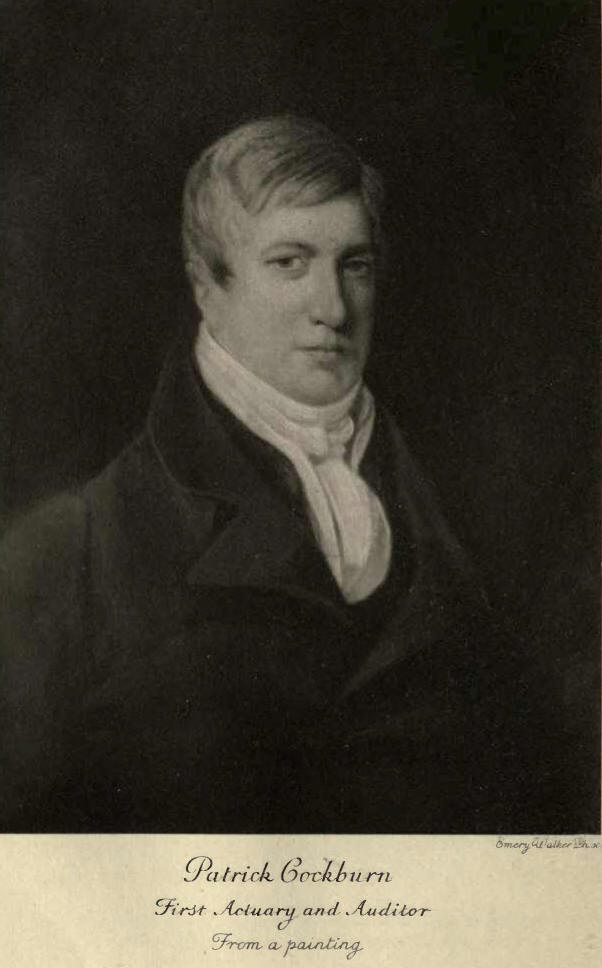

Specimen tables, drawn up by Mr. Patrick Cockburn,

accountant, and founded on the Northampton tables of probability, were

submitted through Lord Primrose to Mr. Morgan, actuary of the Equitable

Society, for revision, to be circulated with the prospectus.

The note contained an invitation to the public to

consider the proposed scheme, and communicate any observations thereon to

Messrs. Gibson, Christie, and Wardlaw, or Mr. William Wotherspoon, and

concluded with the reminder (prudent in days when postage fees were heavy

and had to be defrayed by the addressee) "Letters on this business are

expected to be post paid."

Hitherto all existing assurance offices had based

their calculations on the Northampton tables of mortality, reckoning.

interest at 3 per cent. Mr. Patrick Cockburn, however, to whom was

entrusted the task of framing annuity tables for the nascent Society,

while adopting the Northampton tables, calculated the value of money at 4

per cent and added a fractional sum to the price of annuities to meet the

expenses of management.

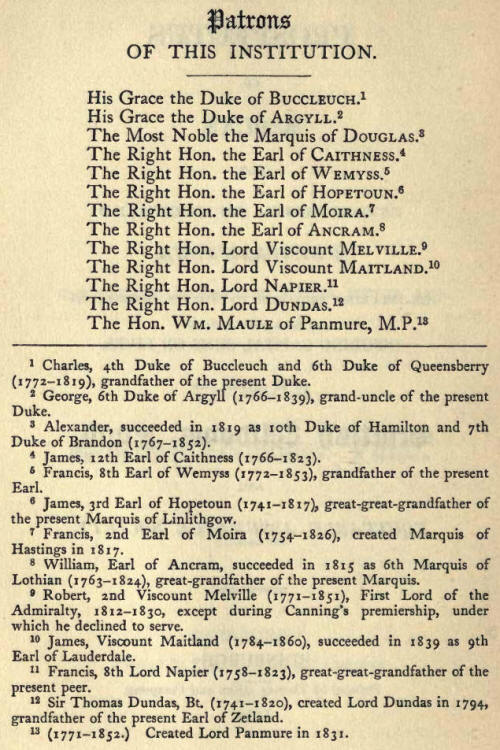

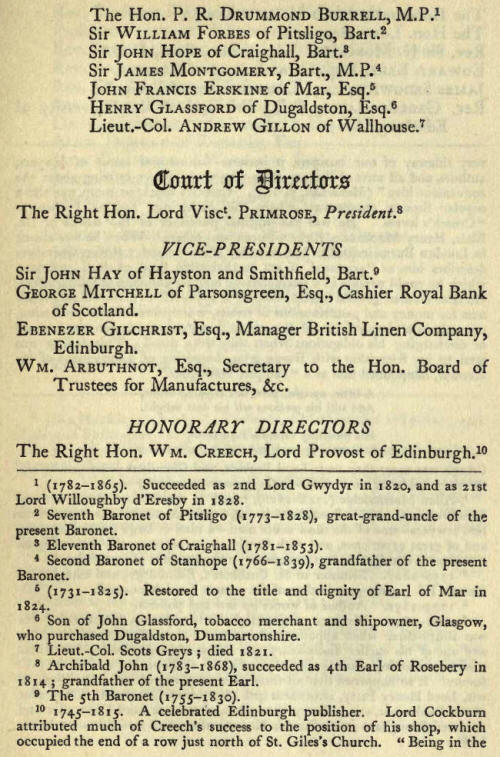

Moderate as was the language of the prospectus, and

modest the scope of the undertaking described therein, there was something

to inspire awe in the list of "eminent characters" whose countenance the

Committee secured and whose support they hoped for. Indeed the names

associated with the enterprise and circulated with the prospectus were so

numerous and so august as might have suggested some risk of overcrowding

the quarter-deck of the craft about to be launched.

annuities to persons to commence in the middle or

later periods of life, and for assuring capital sums payable at the death

of the members, tables of premiums for these different kinds of assurance

had also been calculated by Mr. Cockburn and circulated alongst [sic] with

the prospectus, in order that the opinion of the public might be obtained

with regard to the propriety of this measure." Thereupon the Committee

instructed Messrs. Gibson, Christie, and Wardlaw to frame the Articles of

Constitution so as to embrace these objects.

The preliminary expenses, including printing,

postage, etc., now claimed attention ; and it was resolved that a

subscription list should be circulated among the patrons, proposed

directors, and other friends of the Institution, the sums subscribed to be

repaid on the tontine principle at the first or second decennial

investigation, should the Society find itself with a sufficient balance at

its credit.

The next step was for Messrs. Wardlaw, Cockburn, and

Wotherspoon, the chief promoters of the enterprise, to go to London for

the purpose of consulting Mr. Morgan of the Equitable, whose good offices

had been secured through Lord Rosebery. [Appears in the pro' pectusas

President under the title of Lord Primrose. He succeeded as 4th Earl of

Rosebery on 25th March 1814.] They started on their journey early in

1813—a journey, be it remembered, under very different conditions from the

luxurious transit to which the present generation are accustomed. John

Loudon Macadam had not yet exercised his magic on the North Road; none but

heavy stage coaches could travel on that unmetalled highway, and even if

the deputation travelled by post-chaise, the journey from Edinburgh to

London occupied four or five days. However, it proved well worth the time

and expense; Mr. Morgan put his unrivalled experience freely at the

disposal of the travellers, certified Mr. Cockburn's tables as sound, and

carefully revised the draft articles of constitution.

More than a year passed before the Committee met

again. The truth is that, despite the imposing array of patrons and

officials, honorary and executive, whose names had been published with the

prospectus, the Scottish public had showed no signs of being enamoured of

the scheme; so that at a general meeting of "the friends of the proposed

Institution, to be called the Scottish [sic] Widows' Fund and Life

Assurance Society," held in the Royal Exchange on 6th July 1814, the

Committee had to report that they had been able to raise no more than £248

: 17s. 10d defray preliminary expenses, which was quite inadequate for the

purpose. [Further subscriptions raised the amount to £375 : 18s., which

was repaid to the subscribers at the first investigation in 1825.] This

discouraging circumstance notwithstanding, the meeting (number present not

recorded) unanimously resolved to go forward, and an

Dr. Johnston having been called to the chair, it was

in keeping with the spirit alike of the age, of the nation, and of a city

whose pious motto is Nisi Dominus frustra, that he opened the proceedings

with prayer. The first resolution submitted was passed unanimously,

declaring that the Society was now formed and that the directors were

ready to undertake their duties. At a subsequent ordinary meeting of

directors held on 6th March 1815 it was resolved that, in order to prevent

any disputes that may afterwards arise as to the period of the

commencement of the Society, according to which the periods of

investigation will be afterwards regulated," a standing order should be

enacted that the Society commenced on the 2nd day of January 18 15 (the

1st January being a Sunday), and that the first period of investigation

and distribution of surplus should be on 1st January 1825 or the first

lawful day thereafter.

This resolution having been confirmed by an

Extraordinary Court on the ist May following, it may be argued that the

2nd January is the right anniversary of the Society ; but, although it is

within the power of an Extraordinary Court to rescind one of its own

resolutions, it cannot annul a fact;

Not Jove himself upon the past hath power;

wherefore the true historic natal day of the

Scottish Widows' Fund Life Assurance Society must be held to be 29th July

1814, although for administrative purposes the anniversary falls on ist

January. August analogy to this duplicate observance may be found in the

official date of the Sovereign's birthday, which does not always coincide

with the day of his birth.

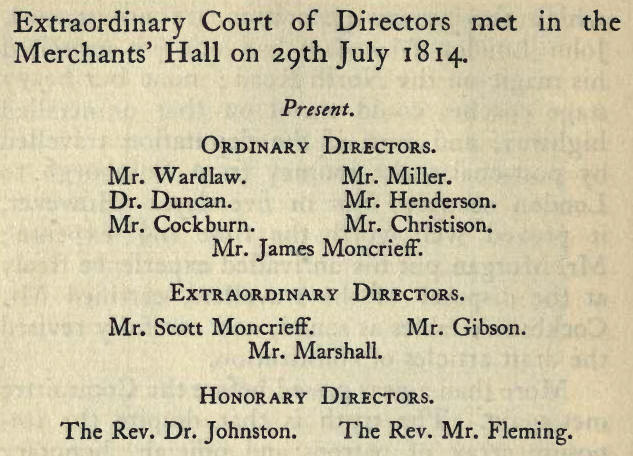

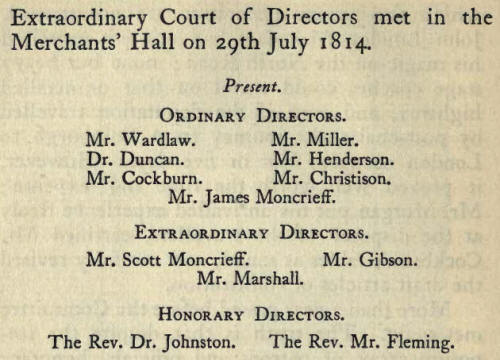

It was also at this Extraordinary Court of 29th July

1814 that Mr. Wotherspoon is first mentioned in the minutes as Manager. He

was called on to find security for the sum of £500.

On 19th September 1814 Mr. Wardlaw applied for a

policy of assurance for £1000 payable at his death, Mr. Cockburn for a

similar one of £500, and the proposals of these gentle-men were accepted

on ioth October following. A number of other policies were issued before

the close of the year, whence it is evident that the Society was in active

existence for five months before its official birthday.

Mr. Morgan of the Equitable Society, having

considered the proposed tables afresh, wrote on 20th September expressing

the opinion that single premium payments, endowment assurances, and

deferred annuities would not be much in request. "The less of this

business you have the better, for if you gain money on one kind of

assurance in consequence of the probabilities of life being higher than

the Tables make them, you must lose in proportion by those assurances

which are advantageous only in proportion as the probabilities are lower

than the Tables make them."

Before receiving Mr. Morgan's letter the directors

had resolved that io per cent be added to the contributions of persons

subject to gout. The Equitable charged ii per cent extra for gout, and the

same for not having had smallpox. "Gang warily" still continued to be the

axiom of the directors, and on 31st October they determined that, until

the funds of the Society should amount to £3000, in the case of any

assurance over £500 being effected upon a life, the amount in excess of

that sum should not be exigible until five years after the date of the

policy, the balance unpaid carrying interest. On 19th December it was

resolved that "in the infant state of the Society it should avoid any

risque of more than common hazard," but recommended that efforts be made

to obtain such data as would enable them to assure persons going outside

Europe, and military and naval men, on terms proportionate to the extra

risk.

Although the Scottish Society was avowedly framed on

the lines of the Equitable, there was a certain divergence between the

immediate aims of the two institutions ; for whereas the Equitable dealt

primarily and almost exclusively with life assurance pure and simple, the

dominant purpose of the founders of the Scottish Society was to raise a

fund securing annuities to the widows of its members. Life assurance only

came to be contemplated as a subsidiary supplement to what was intended to

be the main business, and this was clearly indicated in the title

"Scottish Widows' Fund and Life Assurance Society"; but it very soon

became apparent that the annuity branch of the concern was to be far

outstripped by the assurance of capital sums on lives. Yet the old name,

shortened colloquially into "Scottish Widows," still remains unchanged

—long may it so continue! though one may smile sometimes when some

Englishman, who has neither perpetrated, nor doth contemplate, matrimony,

speculates vaguely on the relevance of the title ; just as one may hear

uninstructed comment upon the name British Linen Bank, an institution

which assuredly has nothing flimsy in its constitution.

It probably cost the founders of the Scottish

Society many an anxious thought when they saw the bulk of their business

flowing from the first into that channel which they had designed as the

less important of the two. They had adopted as a cardinal principle the

mutual system which the Equitable Society had carried to such signal

success, and they had calculated on being able to accumulate a fund by the

sale of annuities. But it soon became evident that they would have to rely

chiefly upon annual premiums on life assurance for building up that fund—a

slow process which might be swamped by the emergence of a heavy claim or

claims before there was enough money at the Society's credit to meet the

same. It was doubtful whether the banks would allow an overdraft upon the

accounts which had been opened; for, as a mutual institution whereof each

member was liable for no more than his covenanted contribution, they had

no share capital—no guarantee from a body of proprietors such as the

managers of a proprietary office might fall back on. Howbeit, fortune

smiled upon the enterprise ; no claim for a capital payment emerged until

the Society had been doing business for eighteen months, and the critical

early months were passed in safety. |